Temple University

Department of Economics

Economics 92

Principles of Microeconomics (Honors)

Directions: You must do all the questions of all parts of the exam. Do your work on this exam. Point values are shown. This is a closed book exam, except for the single sheet of paper you were permitted to bring with you. You may neither give nor receive help.

Multiple Choice (20 points):

1. Suppose a firm maximizes profit by producing 500 reels of video tape. An escalator

clause in their lease kicks in and their fixed costs go up. In order to continue

maximizing profits the firm should:

a. Produce less than 500.

b. Produce more than 500.

c. Continue producing 500.

d. Cut total variable costs by laying off workers.

e. Cut marginal costs by laying off workers.

2. Marginal revenue is defined as:

a. A change in quantity demanded generated by a change in price.

b. A change in price generated by a change in quantity demanded.

c. A change in total revenue generated by a change in quantity.

d. Total revenue divided by quantity.

e. Quantity divided by total revenue.

3. Economists make a distinction between the short and the long run. The difference is

that in the short run, as opposed to the long run:

a. All factors of production are variable.

b. All factors of production are fixed.

c. Only constant returns to scale are possible.

d. Labor productivity is maximized.

e. The law of diminishing marginal returns takes effect.

4. Which activity involves a nonrenewable resource?

a. Eggs used in baking a cake.

b. Corn used to feed hogs.

c. Copper tubing used in residential construction.

d. Hot water used in commercial launderies.

e. Lumber used in residential construction.

5. Coral N. Rocks is shipwrecked on a Pacific atoll and realizes that to survive she

must pick mangoes. She discovers that she has picked more mangoes in the first week of her

labors than in the second since she must climb ever higher in the trees to get the fruit.

Coral has just learned:

a. Engel's Law.

b. The law of opportunity cost.

c. The law of increasing costs.

d. The law of scarcity.

e. The law of production possibilities.

6. Operating inside a society's PPF is a

a. way to stimulate economic growth

b. result whenever the capital stock depreciates rapidly

c. drawback of capitalism relative to socialism

d. sign that population is outstripping the food supply

e. symptom of inefficiency

7. If Jill's demand price for a mountain bike exceeds the $500 price tag, then

a. Jill will purchase the bike

b. Mountain bikes are an inferior good

c. Jill will not purchase the bike

d. Mountain bikes are a normal good

e. Surpluses of mountain bikes are likely

8. If price cuts in video recorders cause expanded cable TV hookups, these are

a. luxury goods

b. substitute goods

c. normal goods

d. inferior goods

e. complementary goods

9. Market prices that are below equilibrium tend to create

a. surpluses of the good

b. declines in resource costs

c. pressures for research and development

d. shortages of the good

e. buyers' markets

10. National income booms from $3.75 trillion to $4.25 trillion and new car sales rise from 3 million to 5 million cars annually. The income elasticity of demand for cars is

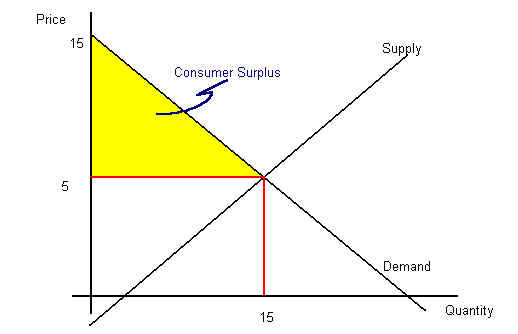

Problem 1 (20 points) Y. Doan Giabuzoff has studied the market for infrared

computer mice. She has determined that the demand curve for such devices is ![]() where Q is quantity, P is price and A is advertising. In the most

recent year advertising was 100. The supply curve is P=.4Q-1.

where Q is quantity, P is price and A is advertising. In the most

recent year advertising was 100. The supply curve is P=.4Q-1.

Use this space to draw a sketch to help you clarify what you are doing. I will not grade this sketch.

21.5-1.5P+1=2.5P+2.5

20=4P

P=5, then Q=22.5-1.5(5)=15

Q=21.5+1-1.5P or P=-2/3Q+15

Consumer Surplus=.5(15)(10)=75

c. What is the elasticity of supply at the equilibrium?

Problem 2 (30 points) About 2000 years ago Peter had a commercial fishing boat that he operated by himself. He had to make a mortgage payment on the boat and each year he painted the bottom. With a little research he was able to figure out the opportunity cost of his time and constructed a cost schedule for the annual operation of the enterprise. I.M.A. Digger, the archaeologist who discovered the fragments of the clay tablets on which Peter kept his records, has come to you for help in reconstructing Peter's work. What Digger has brought to you is shown below.

| Quantity of fish | Total Cost ($) | Marginal Cost | Average Variable Cost | Average Total Cost |

| 0 | 2,000 | - |

- |

- |

| 1000 | 2,340 | .34 | .34 | 2.34 |

| 2000 | 2640 | .30 | .32 | 1.32 |

| 3000 | 2900 | .26 | .30 | .96 |

| 4000 | 3,140 | .24 | .285 | .785 |

| 5000 | 3400 | .26 | .28 | .68 |

| 6000 | 3,750 | .35 | .29 | .625 |

| 7000 | 4200 | .45 | .31 | .6 |

| 8000 | 4800 | .6 | .35 | .60 |

| 9000 | 5550 | .75 | .39 | .62 |

| 10000 | 6450 | .9 | .445 | .645 |

| 11000 | 7,500 | 1.05 | .5 | .68 |

| 12000 | 8,700 | 1.2 | .56 | .725 |

| 13000 | 10100 | 1.40 | .62 | .77 |

| 14000 | 11700 | 1.60 | .69 | .83 |

| 15000 | 13500 | 1.8 | .9 | .9 |

2000

c. At what level of output does the enterprise begin to experience diminishing marginal returns to its variable inputs?

Beyond Q=4000

d. At what level of output does the firm begin to experience decreasing returns to scale?

Can't tell from this short run table.

e. Below what price will Peter not be able to breakeven?

.60, at Q=7k - 8k

f. Below what price will Peter not even drop a hook in the water (i.e., below what price will he shut down)?

.28, at Q=5k

Short Essay: (10 points) Will we ever 'run out of' oil? Use the tools of economics to explain in two or three sentences.

This is right from the Gottheil text. No, we will never run out. Prices ration goods and services. As the supply curve shifts upward, the market clearing price increases and quantity traded decreases. As prices shift upward, substitutes for oil are found.

Longer Essay: (20 points) O. Pinion, a lobbyist, believes that the highways are too crowded, insurance rates are too high, and teen driving mortality rates are too high. What public policy regarding teens and cars will Pinion advocate in his contacts with state legislators. Use the tools of economics to argue your position. Graphs might make your answer more cogent.

There are two parts to a good answer: Factors which shift the supply of miles driven by young drivers, and factors which shift the demand for miles driven by young drivers. In the first set of factors one could include a change in the driving age, or probationary restrictions on teen driving. In the second set of factors one could include insurance surcharges on policies covering teens, or surcharges for gasoline used in cars driven by teens.